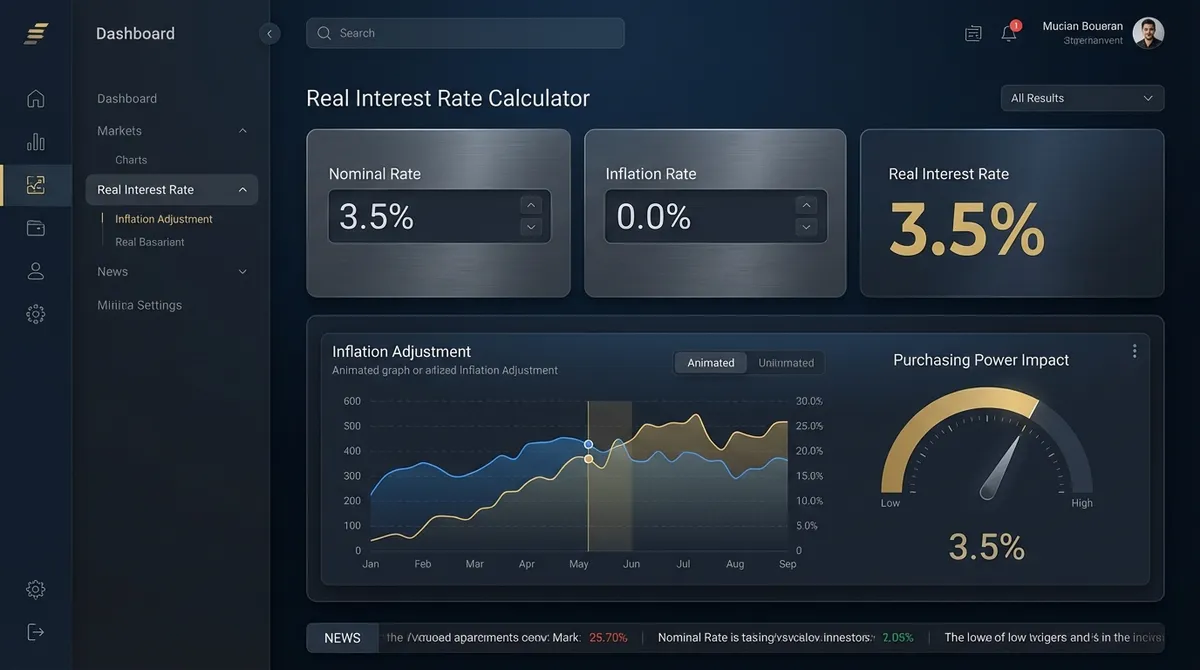

Understanding Real Interest Rates: A Complete Guide

When you see a savings account offering "5% interest" or a loan with "7% APR," you are looking at the nominal interest rate—a number that does not tell the whole story. The real interest rate calculator reveals what your money is actually worth after accounting for inflation, giving you the true measure of your investment's purchasing power or a loan's real cost.

What Is a Real Interest Rate?

The real interest rate represents the true return on an investment or the real cost of borrowing after removing the effects of inflation. While the nominal rate tells you how many dollars you will receive or pay, the real rate tells you what those dollars will actually buy.

For example, if you earn 5% on a savings account but inflation is 3%, your real return is only about 2%. This means your purchasing power grows by 2% annually, not 5%. Understanding this distinction is crucial for making informed financial decisions about savings, investments, and loans.

The Fisher Equation: Exact vs. Approximate Calculations

Our calculator uses two methods to compute real interest rates, giving you both precision and perspective:

Exact Fisher Equation

Named after economist Irving Fisher, this formula provides mathematically precise results by accounting for compounding effects:

This method is more accurate, especially when dealing with high inflation rates or long time periods. It properly accounts for how inflation compounds over time.

Approximate Method

The simpler approach subtracts inflation from the nominal rate:

While easier to calculate mentally, this approximation becomes less accurate as inflation increases. For inflation rates below 5%, the difference is minimal, but at higher rates, the gap widens significantly.

Why Real Interest Rates Matter

For Savers and Investors

A positive real interest rate means your money's purchasing power is growing. If you are earning 6% nominally with 2% inflation, your 4% real rate represents actual wealth creation. However, if inflation rises to 7% while your nominal rate stays at 6%, you are losing purchasing power despite earning interest.

For Borrowers

Real rates determine the true cost of debt. A mortgage at 4% interest with 5% inflation actually has a negative real rate (-0.95% using the exact formula), meaning you are borrowing money that becomes less valuable over time. This benefits borrowers but harms lenders.

For Economic Policy

Central banks monitor real rates closely when setting monetary policy. Very low or negative real rates encourage borrowing and spending, while high real rates promote saving and can slow economic growth.

Common Mistakes to Avoid

Ignoring Inflation Entirely

Many investors focus only on nominal returns. A 10% stock market gain during 8% inflation yields just a 1.85% real return—much less impressive than it first appears.

Using the Approximation for High Inflation

When inflation exceeds 5%, the simple subtraction method can significantly understate the real rate. Always use the exact Fisher equation for accuracy in high-inflation environments.

Confusing Nominal and Real in Planning

Retirement calculators often default to nominal returns. For realistic planning, use expected real returns (typically 4-6% for stocks, 1-3% for bonds) to avoid falling short of your goals.

Practical Examples

Example 1: High Inflation Environment (2022)

During 2022, US inflation peaked around 9% while savings accounts paid 1-2% nominally. This created a real interest rate of -6.4% to -7.3%, meaning savers lost substantial purchasing power even while earning interest.

Example 2: Historical Average

From 2000-2020, US inflation averaged 2.1% while treasury bonds yielded 2.5-3% nominally, providing a modest positive real return of 0.4-0.9%—barely keeping pace with inflation.

Example 3: Deflation Scenario

During deflation (negative inflation), real rates can exceed nominal rates. If nominal rates are 2% and deflation is -2%, the real rate becomes 4.08%—excellent for savers but challenging for borrowers.

Investment Vehicles Designed for Real Returns

While most investments are nominal, some are specifically engineered to provide a guaranteed real interest rate, shielding investors from inflation risk.

Treasury Inflation-Protected Securities (TIPS)

TIPS are US government bonds where the principal adjusts with inflation (CPI). The interest rate is a "real" rate. If a 10-year TIPS yields 1.5%, you are guaranteed to earn 1.5% above inflation, regardless of how high inflation goes.

Series I Savings Bonds

I-Bonds have a composite rate: a fixed rate (real return) plus a variable inflation rate. They are a popular retail instrument for preserving purchasing power with zero nominal risk, though purchase limits apply ($10k/year).

Global Perspective: Real Rates Around the World

Real interest rates vary wildly across borders, driving global capital flows. Investors often engage in strict "carry trades"—borrowing in a currency with low real rates and investing in one with high real rates.

| Economic Scenario | Nominal Rate | Inflation | Real Rate | Impact |

|---|---|---|---|---|

| Emerging Market (High Growth) | 12% | 6% | +5.6% | Attracts foreign capital; currency strengthens. |

| Developed Market (Stagnation) | 0.5% | 1% | -0.5% | Stimulates borrowing; capital leaves (capital flight). |

| Hyperinflation Crisis | 40% | 80% | -22.2% | Currency collapse; panic buying of hard assets. |

Historical Deep Dive: The Volcker Shock vs. Today

To understand the power of real rates, we look to 1980. Inflation was raging at 14%. Fed Chairman Paul Volcker raised nominal rates to nearly 20%. This created a massive positive real interest rate of ~6%.

The Result: The economy entered a recession (short-term pain), but inflation was crushed (long-term gain). Today, central banks try to engineer a "soft landing" by keeping real rates only slightly positive (0.5% - 1.5%), aiming to cool inflation without freezing the economy.

How to Use This Calculator

- Enter Nominal Rate: Input the stated interest rate on your investment or loan (typically 1-15%)

- Enter Inflation Rate: Use current CPI data or your inflation expectation (typically 2-4% historically)

- Add Investment Details: Include your principal amount and time horizon for complete analysis

- Review Results: Compare the exact and approximate real rates, and examine the visualizations

- Analyze Trends: Use the charts to see how inflation impacts your investment over time

Current Market Context

As of 2025, inflation has moderated from 2022 peaks but remains above historical averages. Nominal interest rates on savings accounts have increased, but real returns vary significantly by product. High-yield savings accounts offering 4-5% nominally provide small positive real returns if inflation stays around 3-4%.

However, investors should monitor inflation expectations closely, as rising inflation can quickly turn positive nominal rates into negative real returns, eroding wealth silently over time.

Frequently Asked Questions (FAQ)

Can real interest rates be negative?

Yes, absolutely. If the inflation rate is higher than the nominal interest rate (e.g., you earn 2% interest but inflation is 5%), your real interest rate is negative (-3%). This means your purchasing power is decreasing despite the fact that your account balance is growing in nominal dollars.

Why do banks offer rates lower than inflation?

Banks set interest rates based on central bank policies and market demand for loans, not directly on inflation. During periods of high inflation, savings accounts often lag behind, resulting in negative real returns for savers. Banks have no obligation to beat inflation; their goal is to obtain cheap capital to lend out at a profit.

How does the Fisher Equation differ from simple subtraction?

Simple subtraction (Nominal - Inflation) works well for low rates but becomes inaccurate as rates rise. The **Fisher Equation** `(1 + Nominal) / (1 + Inflation) - 1` accounts for the compounding interplay between the two rates. For example, at 50% inflation and 50% interest, the simple method says 0% real return, but the Fisher equation correctly shows a -33% loss in purchasing power.

Do taxes affect my real interest rate?

They make it worse. You are taxed on the *nominal* interest you earn, not the real portion. If you earn 5% interest and fall in a 24% tax bracket, your after-tax return is only 3.8%. If inflation is 4%, your real after-tax return is actually negative (-0.2%). This "inflation tax" is a hidden cost of taxable savings accounts.

Which assets historically beat inflation?

Over long periods (10+ years), **stocks (equities)** and **real estate** have consistently delivered positive real returns, typically averaging 5-7% above inflation. **Gold** and **commodities** are often used as inflation hedges but can be volatile. **Cash** and **standard bonds** often struggle to keep up with high inflation.

Key Takeaway

The real interest rate calculator transforms nominal numbers into meaningful purchasing power metrics. Always evaluate investments and loans through the lens of real returns to make truly informed financial decisions that protect and grow your wealth over time.