Complete Guide: Working Capital Calculator & Financial Analysis

Working capital is the lifeblood of any business. This comprehensive guide explains how to calculate working capital, interpret the results, and use our working capital calculator to assess your company's short-term financial health and operational efficiency.

Key Takeaway

Working capital measures your company's ability to meet short-term obligations and fund day-to-day operations. A positive working capital indicates financial stability, while negative working capital signals potential liquidity issues.

What is Working Capital?

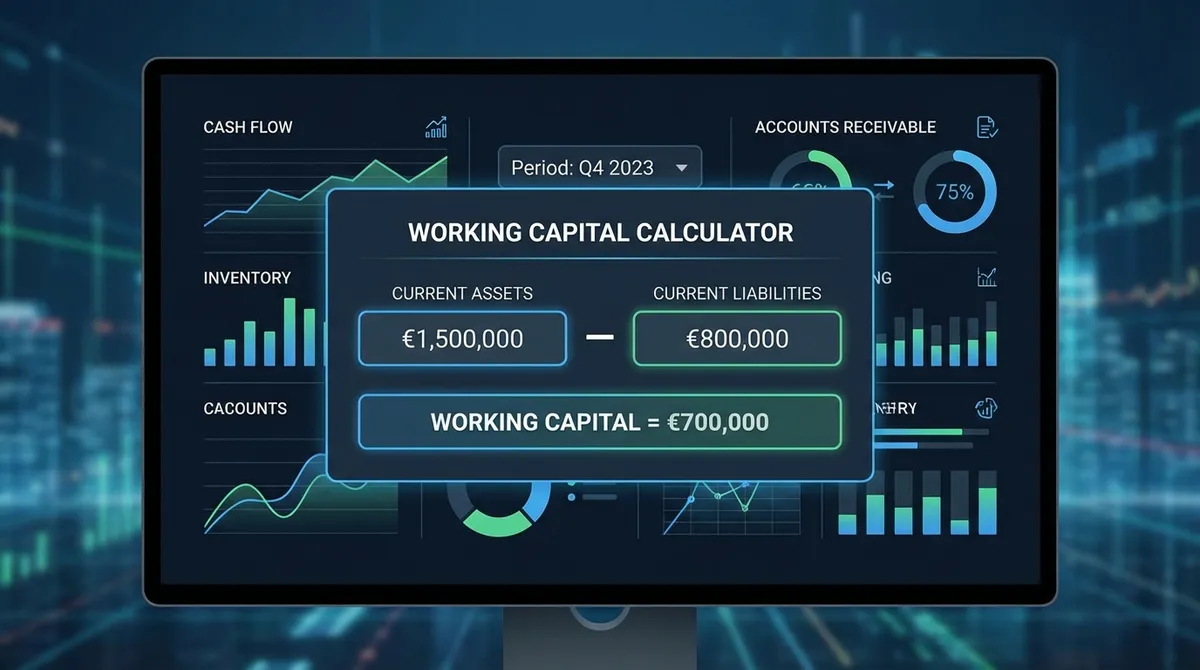

Working capital represents the difference between a company's current assets and current liabilities. It measures the resources available to meet short-term obligations and fund daily business operations.

Simple Working Capital Formula:

Working Capital = Current Assets - Current Liabilities

Why Working Capital Matters

Working capital is crucial for business survival and growth. It impacts:

Positive Working Capital Benefits

- •Ability to pay suppliers and employees on time

- •Flexibility to handle unexpected expenses

- •Capacity to invest in growth opportunities

- •Stronger negotiating position with creditors

Negative Working Capital Risks

- •Difficulty meeting short-term obligations

- •Increased borrowing costs and financial stress

- •Missed growth opportunities

- •Potential business insolvency

Components of Working Capital

Current Assets (What You Own)

Current assets are resources that can be converted to cash within one year. Our calculator includes:

Cash & Cash Equivalents

The most liquid assets including cash in bank accounts, money market funds, and short-term government bonds. This is your immediate spending power for daily operations.

Accounts Receivable

Money owed by customers for goods or services delivered. While not immediately available, these represent near-term cash inflows. Efficient collection is crucial for maintaining healthy working capital.

Inventory

Raw materials, work-in-progress, and finished goods ready for sale. Inventory represents tied-up capital until sold. Balancing adequate stock levels with minimizing holding costs is essential.

Other Current Assets

Prepaid expenses, short-term investments, and other assets convertible to cash within a year. These vary by business type but contribute to overall liquidity.

Current Liabilities (What You Owe)

Current liabilities are obligations due within one year. Managing these effectively is as important as managing assets. You can estimate tax-related liabilities with our Business Tax Calculator:

Accounts Payable

Money owed to suppliers for goods and services purchased on credit. While these represent short-term obligations, strategic payment timing can optimize cash flow without damaging supplier relationships.

Short-term Debt

Loans and credit lines due within one year, including portions of long-term debt. These require careful management as they represent immediate cash outflows that can strain liquidity.

Accrued Expenses

Incurred but unpaid expenses like wages, taxes, and utilities. These ongoing obligations require consistent cash flow to meet payment schedules and avoid penalties.

Other Current Liabilities

Customer deposits, deferred revenue, and other short-term obligations. These vary significantly by industry and business model but impact overall working capital requirements.

Working Capital Ratios & Interpretation

Beyond the basic working capital calculation, financial analysts use key ratios to assess liquidity and operational efficiency. Our calculator provides three critical metrics:

1. Current Ratio

Current Ratio = Current Assets ÷ Current Liabilities

The current ratio measures your ability to cover short-term obligations with short-term assets. You can calculate this specifically with our Current Ratio Calculator.

< 1.0x

Poor - Cannot cover current liabilities

1.0x - 1.2x

Concerning - Tight liquidity

1.2x - 2.0x

Good - Adequate liquidity

> 2.0x

Excellent - Very liquid

2. Quick Ratio (Acid-Test)

Quick Ratio = (Cash + Accounts Receivable) ÷ Current Liabilities

The quick ratio provides a more conservative measure by excluding inventory. Check our Quick Ratio Calculator for a deeper dive.

< 0.5x

Poor - Severe liquidity risk

0.5x - 1.0x

Concerning - Limited liquidity

1.0x - 1.2x

Good - Adequate quick liquidity

> 1.2x

Excellent - Strong position

How to Interpret Your Results

Our working capital calculator provides not just numbers, but actionable insights. Here's how to interpret your results:

Positive Working Capital

Your business can cover short-term obligations and has resources for operations. However, excessively high working capital may indicate inefficient use of resources that could be invested for growth.

Negative Working Capital

Your current liabilities exceed current assets. This signals potential liquidity problems and difficulty meeting short-term obligations. Immediate action may be needed to improve cash flow or restructure debt.

Optimal Range

Most healthy businesses maintain working capital between $50,000 and $200,000, with current ratios between 1.5x and 2.5x. However, optimal levels vary significantly by industry and business model.

Industry-Specific Considerations

Working capital needs vary dramatically across industries. Our calculator includes industry-specific scenarios to help you benchmark against typical patterns:

Manufacturing

Typically requires high working capital due to inventory needs and longer accounts receivable cycles.

- • Heavy inventory investments

- • Extended payment terms

- • High accounts receivable

- • Target ratio: 1.5x - 2.0x

Service Industries

Generally need less working capital due to minimal inventory and faster payment cycles.

- • Low inventory requirements

- • Faster cash conversion

- • Recurring revenue models

- • Target ratio: 1.0x - 1.5x

Retail

Requires substantial working capital for inventory, but may have quick inventory turnover.

- • Significant inventory investments

- • Seasonal demand fluctuations

- • Supplier payment terms critical

- • Target ratio: 1.2x - 1.8x

Startups

Often struggle with working capital due to limited credit history and high growth demands.

- • Limited access to credit

- • High growth capital needs

- • Uncertain cash flows

- • Careful management essential

5 Strategies to Optimize Your Working Capital

1Accelerate Receivables (DSO)

The faster you collect cash, the improved your position. Reduce your Days Sales Outstanding (DSO) by implementing better collection policies.

- Offering early payment discounts (e.g., 2% net 10).

- Requiring upfront deposits for large orders.

- Automating invoice reminders and implementing easier payment gateways.

- Conducting credit checks on new clients to avoid bad debt.

2Extend Payables (DPO) With Care

Hold onto your cash longer by increasing Days Payable Outstanding (DPO). This directly impacts your Cash Flow.

- Negotiate longer payment terms (30 to 45 or 60 days).

- Wait until the due date to pay invoices (automate this to avoid late fees).

- Communicate proactively if you need an extension rather than just delaying payment.

3Optimize Inventory Management (DIO)

Unsold inventory is cash sitting on a shelf. Improve Days Inventory Outstanding (DIO) with our Inventory Turnover Calculator.

- Adopting Just-In-Time (JIT) inventory practices.

- Regularly auditing stock to identify and liquidate slow-moving items.

- Using inventory forecasting tools to prevent overstocking seasonal items.

4Refinance Short-Term Debt

If short-term loan payments are choking your cash flow, consider refinancing. Learn more about working capital strategies on Investopedia.

5Review Expenses Frequently

Conduct quarterly audits of all recurring expenses. Cancel unused software subscriptions, renegotiate vendor contracts, and eliminate wasteful spending that drains cash without adding value.

Case Study: The Turnaround

Before Optimization

ABC Manufacturing Co. struggled to pay staff despite high sales.

- Current Assets: $500,000

- Current Liabilities: $480,000

- Working Capital: $20,000

- Current Ratio: 1.04

The company was one late customer payment away from insolvency.

After Strategy Implementation

They refinanced debt & automated collections.

- Current Assets: $550,000 (+ Cash)

- Current Liabilities: $350,000 (- Debt Refi)

- Working Capital: $200,000

- Current Ratio: 1.57

Considerable safety margin achieved within 6 months.

Frequently Asked Questions (FAQ)

Can working capital be too high?

Yes. While positive working capital is good, having an excessive amount (a current ratio over 3.0) might indicate that the business is hoarding cash instead of investing it back into growth, R&D, or paying dividends to shareholders. It suggests inefficient capital allocation.

How does seasonality affect working capital?

Seasonal businesses (like landscaping or retail) see wild swings. A toy store might have huge inventory (asset) and debt (liability) in October, but high cash and low inventory in January. It's crucial to analyze working capital year-over-year (e.g., this January vs. last January) rather than month-to-month to spot true trends.

What is the difference between Net Working Capital and Gross Working Capital?

Gross Working Capital refers simply to the company's total current assets, disregarding liabilities. Net Working Capital (what this calculator shows) is Current Assets minus Current Liabilities. Net Working Capital is the far more useful metric for assessing true financial health.

Does a line of credit count towards working capital?

An unused line of credit does not appear on the balance sheet, so it is not in the standard calculation. However, it is a critical source of "secondary liquidity." The used portion of a line of credit is a current liability and decreases your working capital.

Pro Tips for Accurate Results

- •Update figures monthly for trend analysis and early problem detection

- •Compare results to industry benchmarks for meaningful context

- •Calculate working capital regularly to track improvements or deterioration

- •Use the export feature to save results and share with stakeholders